The inflation sledgehammer

and what you need to watch for in tech and crypto

When I was 16, I was super proud of passing my driving test quickly after my birthday. It wasn’t because I was some natural-born driver. It was because I was fortunate that, from the age of 15, my Dad would let me park his car every night on our driveway, which was very steep. I realised that driving a car was all about knowing the biting point on the clutch. Once you have mastered that, the rest was easy.

The Fed is about to end its 18-month experiment of pouring rocket fuel on the most significant monetary stimulus the world has ever seen. Will rates have an impact and how are markets positioned? Given just how much impact macro is having on crypto and tech, I needed to answer these questions for myself and started making notes that I am sharing below.

TLDR: The market is very scared inflation will persist and Fed rate rises may not impact some major sources of inflation. However, a turn in the second derivative of inflation combined with light positioning in growth could mark the bottom.

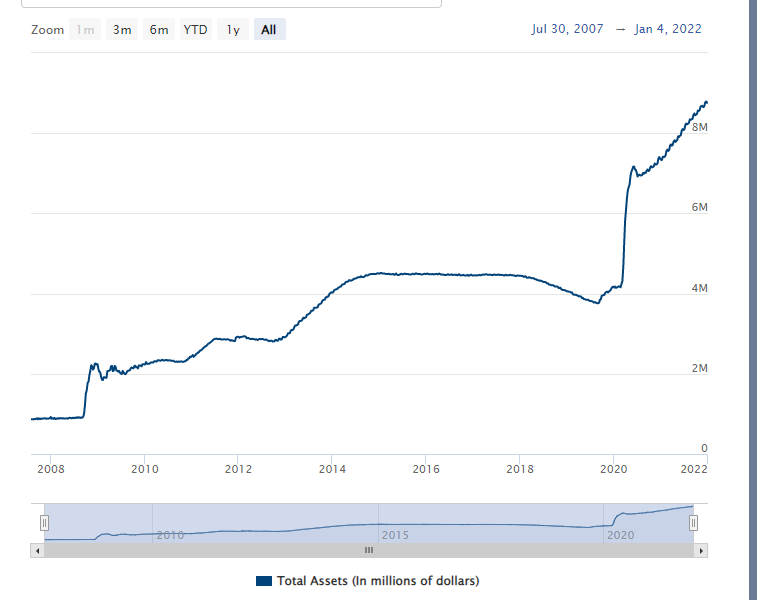

Fed Reserve Balance Sheet

Source: https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

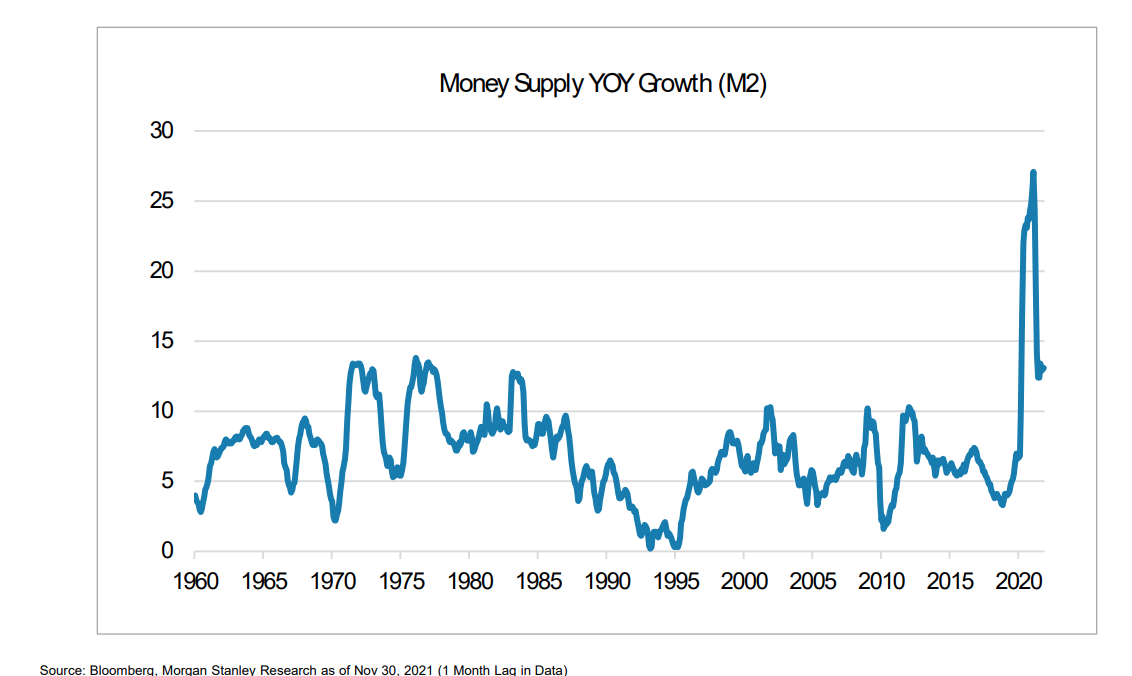

The explosion in the Fed’s balance sheet has (unsurprisingly) unleashed inflation worldwide. Most participants in the financial markets have never seen inflation in their careers, let alone have a playbook on how to deal with it.

Whilst the US Money supply is reversing course, it is too little too late. The inflation touchpaper has been lit.

Last Jan, the market had assumed that the Fed wouldn’t raise rates until 2024; now the market is almost certain it will raise rates by March. The rise of interest rates globally is not just a US trend; markets are implying 100bp of rate hikes over the next 12 months in the UK, 139bp in Canada, 245bp in Mexico, 150bp in Poland and 145bp in New Zealand. Japan stands out as the only major country without a rate hike priced in for 2022.

Many growth stocks have been decimated, and crypto this weekend finally cracked, with ETH touching 3k and BTC almost touching 40k.

Is there any good news? Yes, potentially.

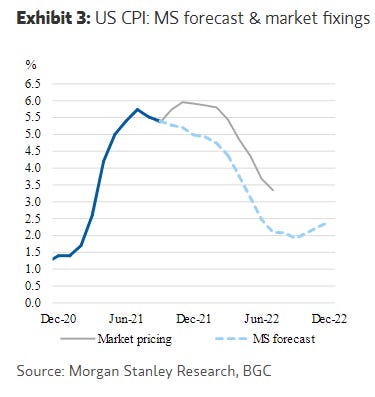

US Consumer prices may well have peaked. Morgan Stanley is forecasting a more doveish scenario than the market.

The problem central banks face is that causes of inflation are not easy to fix with monetary policy alone.

Supply chain - Unlikely to be fixed this year

COVID is impacting labour availability from ports to factories globally. Omicron is going to continue to roll across the world meaning the supply chain will find it hard to coordinate.

China has a whole host of issues.

Shutting down manufacturing and shipping hubs due to their COVID zero strategy

Sanctions on export regions such as Xinjiang cotton (produces 85% of China’s cotton). Cotton prices are at 5-year highs

Over-reliance on companies on just-in-time parts means the system is a mess. Most of the experts think we will normalise sometime in 2023 maybe even 2024. The good news is that much of this is demand-led, so if we see real demand destruction, maybe this will accelerate the easing of prices.

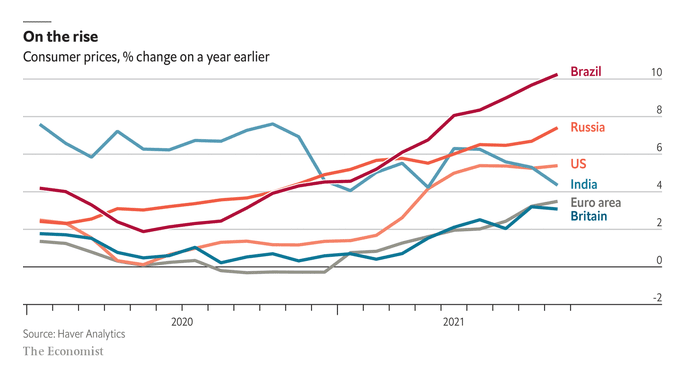

Food inflation is a headache

source: https://twitter.com/Trinhnomics

Gas prices are being squeezed by Russian policy. Next few months negotiations on Ukraine will set the tone for where gas prices go from here. Supply chain issue, Thai Pork curbs, Indonesian coal and Palm oil problems are going to continue to ripple through food markets.

Wage inflation - Unlikely to be fixed this year

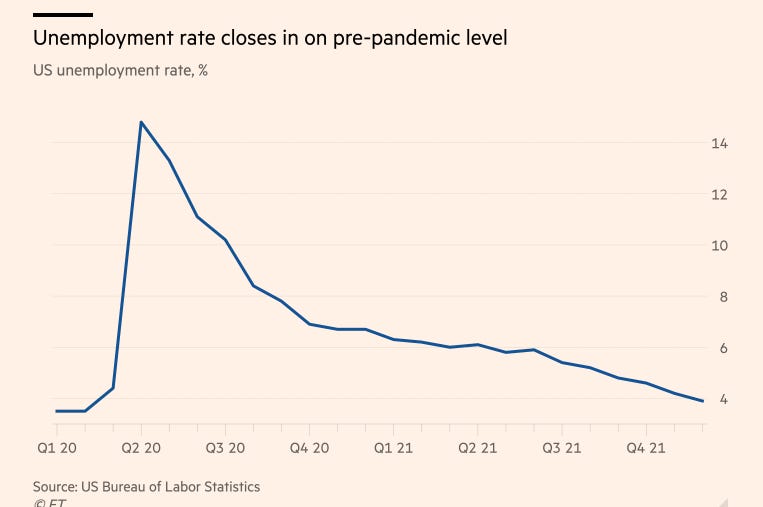

US unemployment is at pre-pandemic levels. The great resignation and displaced labour forces means that the job market is as hot as anyone has seen it ever. Wage inflation is rampant, and wage inflation tends to be sticky and moves across the economy (If someone is hired to do the same job as you and is paid more, then people either leave or ask for more money).

Businesses have learnt a vital lesson. Do not fire too quickly. COVID was initially secretly celebrated as a way to cut the workforce and improve margins. That is why today, S&P 500 margins are 18.8% which is near record highs. However, whilst productivity improvements helped to start with, demand is strong that everyone is hiring, and there simply aren’t enough skilled staff to cope. Technology can only help you so much.

Rents are rising

NY City rents are back to pre-pandemic highs. Despite potentially rising rates, we haven’t seen mortgage rates rise. Real assets are traditionally an inflation hedge, and you could continue to see them move higher, which pressures rents further. The challenge with rent rises is that they can sustain.

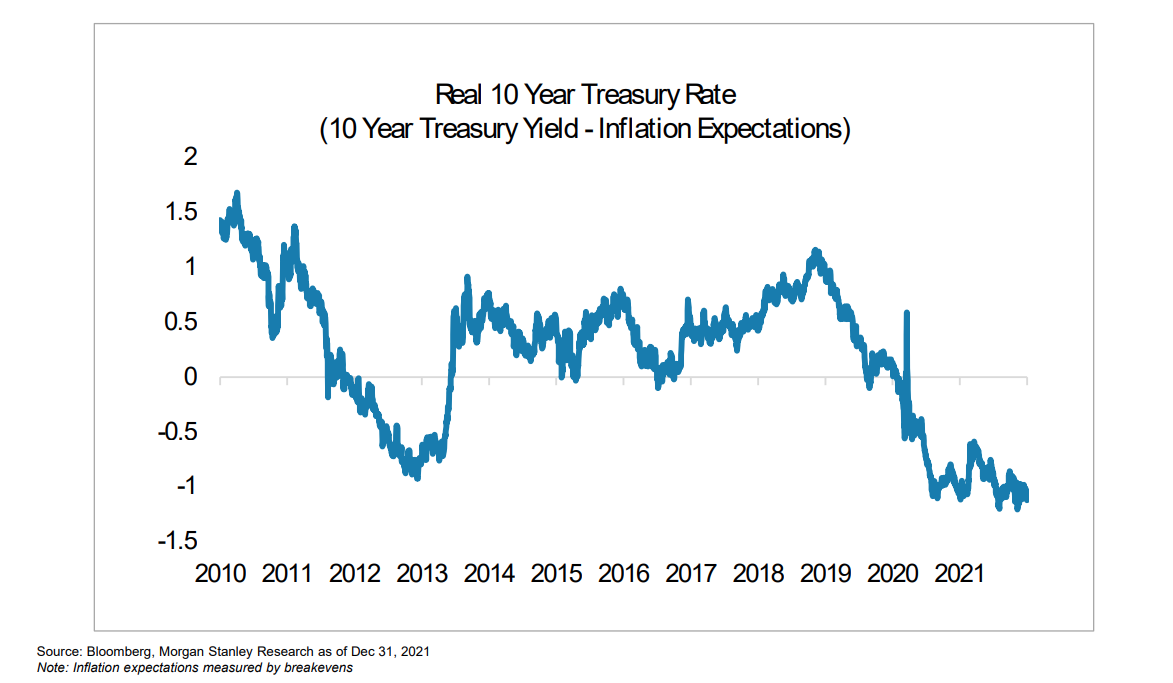

Rates are still highly negative

The real problem for central banks is twofold: (1) can you tame inflation expectations with rate rises. Supply-side cost inflation can only be tackled with demand destruction in the short term (2) How far do rates need to rise?

As we can see in the chart above, with inflation likely to rise to 7% on Wednesday’s print, even 3 rate rises won’t be enough to bite.

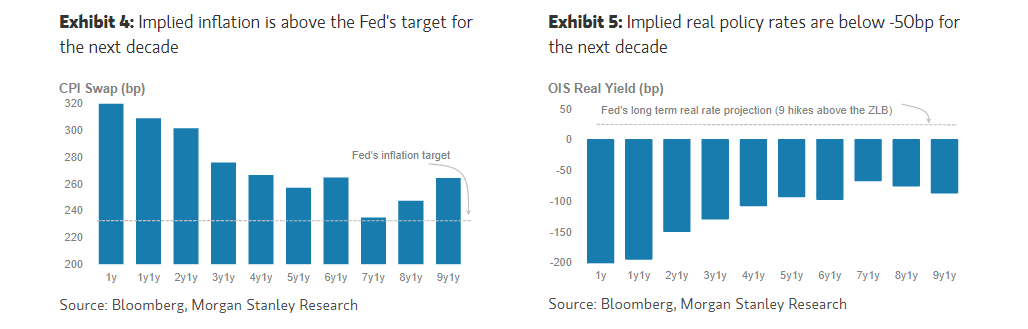

Markets are currently assuming that inflation is going to above the Fed’s target for the next 10 years(!).

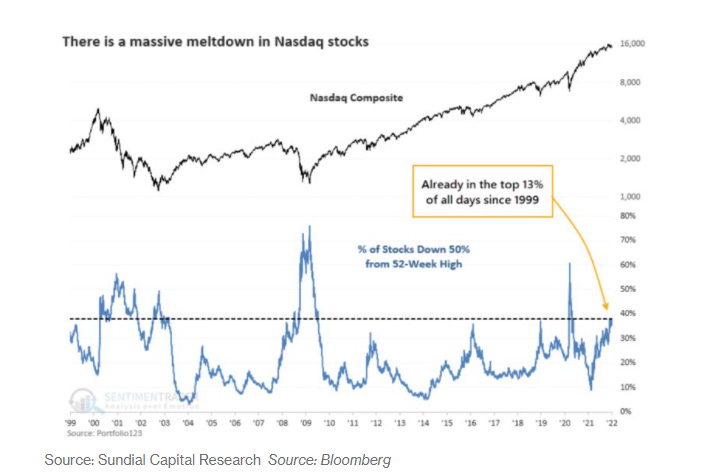

Tech Valuations and positioning

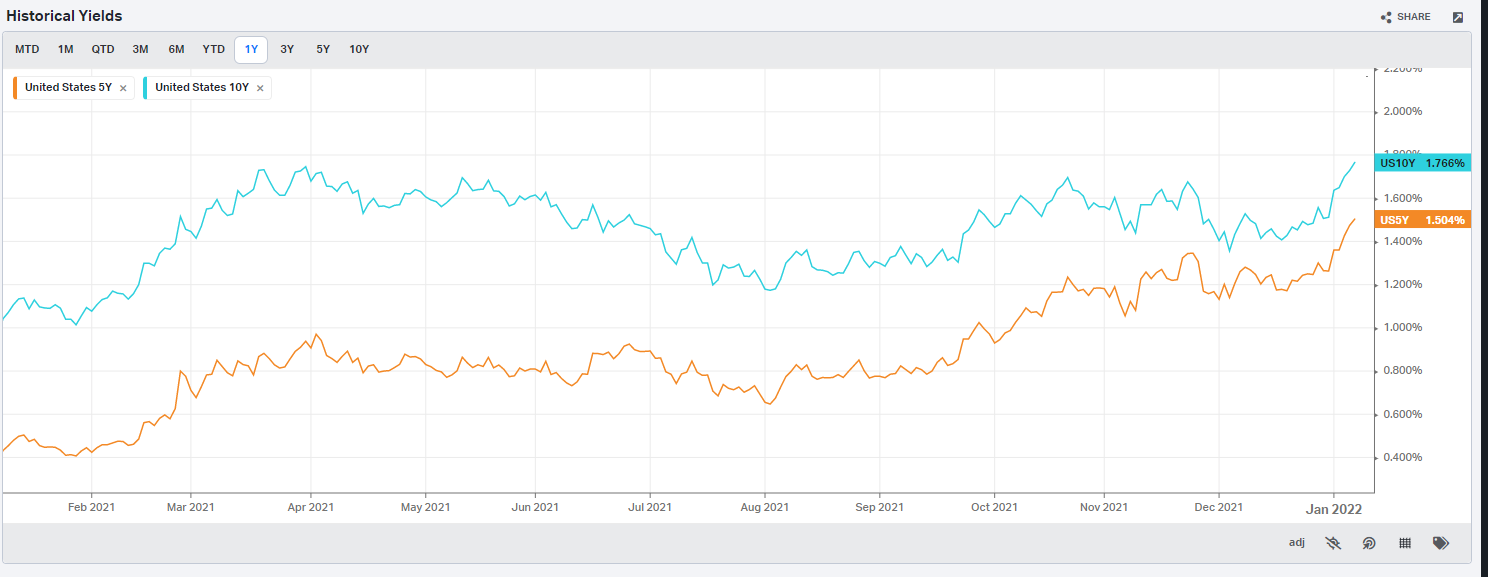

The US 10 year has started to break higher but not necessarily because people are expecting stronger growth in the future, but purely reacting to higher inflation. Again, this is unchartered territory now for tech.

And unsurprisingly, tech is correcting. However, greed and fear indices across the board are screaming capitulation, so what do we need to look for next?

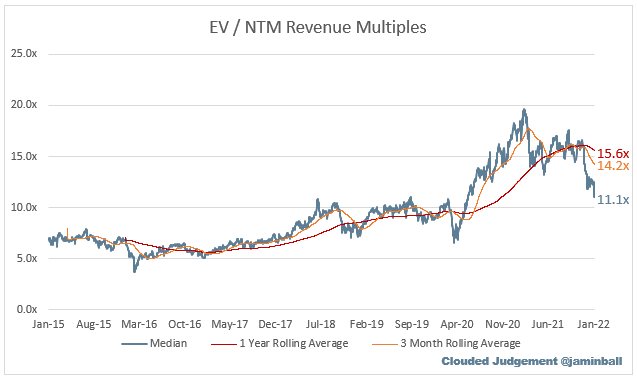

SAAS Multiples

And unsurprisingly tech has corrected. Jamin Ball , who focuses on high growth software, says that on a like-for-like basis we are now at a 27% premium to pre-covid highs. Given the huge adoption of tech that we have seen globally, I can’t see pre-covid valuations as the base case valuation target, so we must be closer to the bottom than the start.

source: https://twitter.com/GavinSBaker

MS’s Quant team confirm that we are 85% of the way through the downside move for a rate shock in their Crowded Longs (CRWD) and Expensive Tech (EVSA) baskets.

source: https://twitter.com/GavinSBaker

Looking at positioning, GS hedge fund data shows that we are at 5 year lows in terms of ownership of growth stocks

However, greed and fear indices across the board are screaming capitulation, so what do we need to look for next?

What to watch out for

Any signs that the second derivative of inflation has turned will calm the market (this is key for the near term)

→ CPI doesn’t trend higher for 2-3 monthsShipping rates / Supply chain bottlenecks easing

→ Shipping rates falling from these levels and post congestion easingMortgage rates reacting to Fed moves and cooling the housing the market

→ End of very LTV offers. House prices in suburban areas cooling

What could derail us further?

Sell off moving out of high growth names affecting the broader market

→ If we see money leaving equities and moving to cash/bondsUS govt chatter of price controls getting louder

→ Any move by Congress to control pricesInflation continues to spike in the March fed meeting (do we get more than 3 rate hikes?)

One thing I had learnt whilst trying whilst hill-parking my Dad’s car was that the biting point of a 10-year old Volvo can be a surprise to those not used to finding it. With real rates so negative, if inflation persists, the biting point at which rates start to impact real assets could be a lot higher. The optimist in me looks at second derivatives, valuation and positioning to say we are closer to the end of the washout than the start.

In the meantime, everyone, please keep yourselves and your loved ones safe!