The end of public OR private investing

Welcome the crossover fund

The pendulums of investing tend to swing from one extreme to another. Today we are coming off a multi-decade old mantra that staying private for longer is best for entrepreneurs and their companies. The idea is that private venture capital is patient, long-term capital that is not subject to the wild swings of public markets. During COVID when most VC’s ran for the hills (for a while) public markets funded record-breaking debt and equity raises. VCs promises rang very hollow.

Startups staying private for a decade or longer seems to be normal today but this wasn’t always the case.

Internet 2.0 companies were going public as soon as two years old. Amazon IPO’d at a valuation of $438mln. Today, most bankers would advise you not to list even if you are under $1bln as it would be considered a micro-cap in the US. At the time that Amazon, Google, etc went public, they were granted a valuation premium to their private round valuations. This is normal as there should always be a discount for private companies as their shares are illiquid.

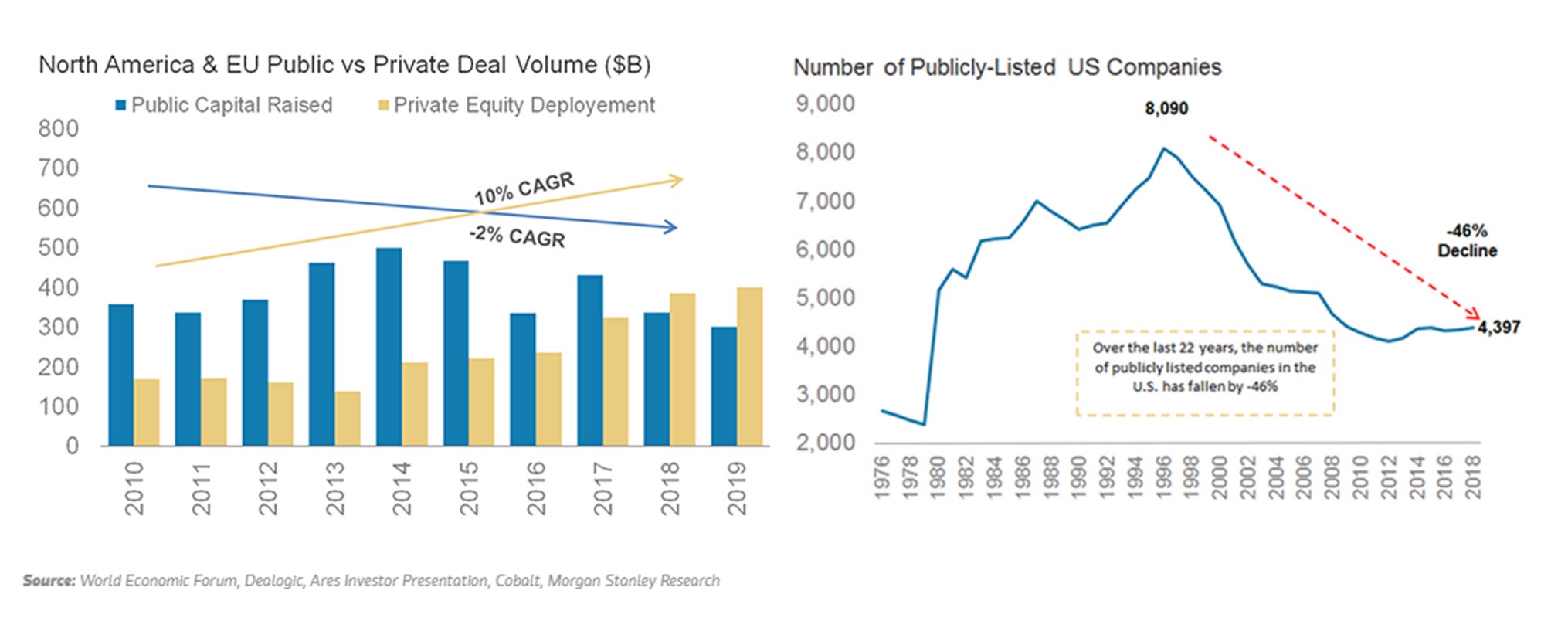

During the boom of venture capital in the US, the amount of money pouring into private capital skyrocketed and the number of publically listed companies collapsed to levels we have seen since the 70s. During these boom years, there were many times that private market valuations exceed public markets which doesn’t make sense in the long run. Why did nobody care about liquidity?

Liquidity is a funny concept though. Private markets companies were always told how long and difficult an IPO is (mostly true) but things are now changing. Tech companies have realized that the difference between being private and being public can be a 3-month date with a SPAC. Private companies are rushing to IPO to take advantage of what is considered to be a hot market. The attractive valuation jumps in public markets and lack of allocation in hot public deals mean that crossover funds have never been busier. As there is more of a blurring of the lines between what is definitely public and what is private this will only add impetus to the trend. The concept of liquidity can be as fluid as its definition.

Source: FT

Crossover funds like Tiger Global move at lightening speeds and are willing to pay premium valuations which means that they outcompete other traditional growth stage investors. Whilst some VCs bemoan these crossover investors feeding in their backyard as a new phenomenon it isn’t. The move towards private market investing from public portfolios has been increasing for a decade as we can see from the charts above. This is not an insignificant amount of money. If global VC AUM is ~$1trn and in the US it stands at ~$600-700bln, crossover funds are around double digits % of overall investing dollars. That is a big number.

Is it logical for there to be a delination between public and private investing? In 2008, crossover funds were really struggling. They hadn’t really thought about the impact that a run on their public market fund would have on the private market book. When investors asked for their money back, their privates book was suddenly a big percentage of their overall book which forced them to sell these names during a tough market. Today, many lessons have been learnt and structures are now much more conservative in how assets are co-mingled to prevent a repeat of that disaster.

Those that argue that VC and public funds should be kept separate are doing so because they feel the “art of VC” is very different from that of public markets. In early-stage investing that may be the case, but that doesn’t hold true for late-stage or growth investing. Late-stage investing is basically investing like a PE firm, there is a tonne of data available, product and tech risk is minimal. It is about scaling and execution which is the same risk as we look at in public markets.

I would argue that today if you are a public market fund, not doing privates then you are doing a disservice to your LPs. I was just pondering the last couple of areas that we have been doing work on in the last 6 months. In payments - if you want to invest in Stripe or Checkout.com there is no way that one can look at that without also looking at publically listed Adyen. If you want to invest in Coinbase, there is no way that you can make an intelligent investment decision without looking at FTX or Gemini. They are so similar in so many ways, that if your universe doesn’t include them all, it’s incomplete. You are boxing with one and one eye shut.

Today, the public market calendar is busier than ever with companies lining up to go public. This boom isn’t just in the US, but India and HK. We have seen news recently about SPAC regulations being loosened in SG and HK but what regulators should really focus on is easing the regulations that slow down the IPO process. We can still be prudent without asking for a startup to go through a year+ long process in some markets to go public. The shorter the time between public and private whether its through SPACs or looser regulation, the less there will be a difference between public and private. Crossover funds are here to stay and they are only just getting started.

I recently did a live stream with Lynk which you can view here talking about how crossover funds are the future of tech investing, please take a look, happy to hear feedback