Roblox IPO - Cheap creator platform

In this letter, I breakdown the Roblox S1 IPO filing ahead of its blockbuster IPO. This is one of the most impressive creation platforms in the world right now, have a read below to see why

Creator platforms are coming of age. (User-generated content) UGC used to be pictures and videos but increasingly platforms that monetise your creativity in other mediums have been taking off. They all have a similar core product which is to provide tools by which creators can create and then some social network by which those creations are consumed. Youtube, Tik Tok, OnlyFans, Patreon, Substack are in a long line of these excellent businesses. Some that emphasise the social network element take longer to build but once the flywheel is going they become formidable forces to stop. That is where Roblox is today.

The games industry is firmly mainstream. In North America it is worth more than the sports and movie industry combined, reaching $179bln in revenue in 2020. Massively open worlds that previously could only be explored by players and interacted with in the way the game designers meant them to interact with are opening themselves up to be completely customised and designed to something that invokes a completely different experience.

Unity, which IPO'd recently is an example of a dominant gaming toolkit that allows creators to produce games in a realistic 3D world. The stock is up almost 300% since IPO. Unity and Epic (their private rival), both need training and money to get started so there is a barrier to entry. Minecraft (owned by Microsoft) and Roblox are aimed at a younger audience of consumers, portray less sophisticated graphics, are far easier to develop on but each has a powerful social network for the consumers to both discover new games but also to make friends and socialise. This is blurring the line between users and developers and allows any kid or adult with an idea to design, create and get feedback on a game almost instantly.

Roblox filed their S1 late last year but then delayed the IPO to Q1 this year. Ahead of the listing I breakdown some of the key areas of interest. The numbers are impressive and the stock is likely to trade much higher than the mooted $8bln valuation.

History

Roblox was created in 2004 and released in 2006 by David Bazucki and Erik Cassel, sadly Erik passed away in 2013 from cancer. They had created an award-winning physics simulation engine in the 80s on the Mac. David was also the founder of Knowledge revolution, educational software for teaching physics that was later sold to MSC. Whilst at Interactive Physics they started work on Dynablocks which would later be renamed to Roblox (robots & blocks). The very heard of Roblox is about physics and learning all within a social wrapper.

What is Roblox?

Roblox is a game creation engine with a social network in one. In the Roblox platform, users can create games and invite others to play. The Roblox economy is powered by Robux, an in-game currency that users can buy with real dollars. Many of the games are very simple but addictive. Here are the top 3 games in 2020 each of which has been played over 1bln plays

Meep City -A virtual place to hang out customise your real estate

Jail Break - The user can play any number of roles to conduct a heist, break out of jail or play the cops trying to stop the mayhem. This game now also has offline toys

Adopt Me - Pet adoption game

Screenshot of Adopt Me!

Roblox describes their platform in the S1 as "human co-experience". These parallel, virtual universes or Metaverses as they are now called are places that will become a bigger part of all our lives. Younger audiences are completely comfortable with these Metaverses as a place to play, socialise amongst friends or meet new people. They also represent a huge opportunity to monetise attention.

Roblox's numbers are impressive.

75% of Americans between 9-12 years old play its games

36.2 million people DAUs, +82% in the 9 months to Sept 2020

7 Million Active developers

Hours engaged grew 122% to 22.2bln in 9 months to Sep 2020

The average active user spends 2.6 hours a day (this compares to Tiktok at 58 mins, Youtube at 54 mins and Instagram at 35 mins)

54% of users are 12 and under

Takeaway: Kids under 12 are obsessed with the platform. They creating and playing games at an accelerating rate and spending much more time on the platform than any social media and its not even close.

Robux

Roblox mainly makes money from users buying Robux, their in-game currency and then spending them inside the games. For this, they have a 30% take rate. However, if developers want to convert their Robux into USD, they can only do so at 35c in the dollar. Which is why on average developer earnings are only about 17% of sales. Roblox actually pays more to payment processing fees (24%) than their developers. The S1 points out that Robux get recycled within the system as well. Developers can use them others games or to buy more development tools. None the less, this fee is steep and something investors need to watch, as they may get pushback from their developer base at some point. Taking a lot of money from young kids trying to make a dime is a potential PR hot potato.

Revenue

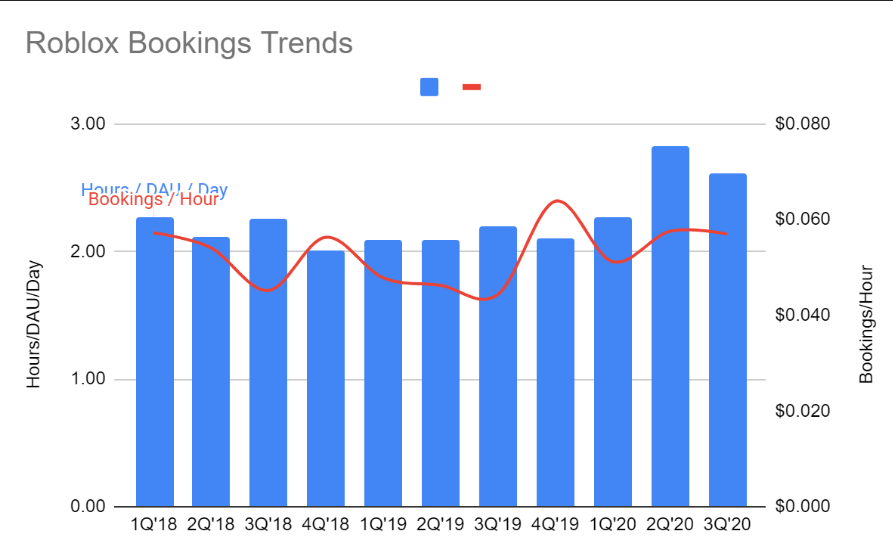

An important point to note here is that revenue is recognised over a period of 23 months as that is the average lifetime value of their customers. Users do, however, pay cash upfront giving Roblox excellent negative working capital cycles. The cash received is categorised under "bookings" and then recognised as revenue over the next 23 months. This means that revenue actually becomes a lagging indicator and bookings are a far more important metric to track. Just like being in a casino, the longer a person is using Roblox the more money they tend to spend. So monitoring hours per DAU per day and then bookings (spend) per hour are the two key metrics to track. You can see below how this spiked during Covid but has held steady but growing (HT to Tremblingwithgreed for raw data)

(Source: S1, tremblingwithgreed)

(Source: S1, tremblingwithgreed)

What is really driving bookings is the huge spike in DAUs and hours engaged. I assume that things will normalise post COVID but will do so at higher levels. Question will be how will the market take a fall in bookings revenue if we are trading at a very rich multiple. In theory, they should expect this if the company guides conservatively but the market sometimes is quite short-sighted.

Other sources of revenue come from a split of the premium subscription-based on time spent and sales of items through the marketplace.

Costs

It is important for us to breakdown the costs and see where the company can get leverage as their business scales.

Cost of revenue - This is depreciation of servers and infrastructure as well as Trust and Safety.

Trust & Safety - was mentioned 44 times in their S1 and is something they will continue to invest and focus on regardless of short fluctuations in revenue.

Sales & Marketing - Not growing as fast as sales and so their marketing is getting more efficient. In the 9 months ending Sept 2020 you can see it went from 8.9% to 7.1% of revenue.

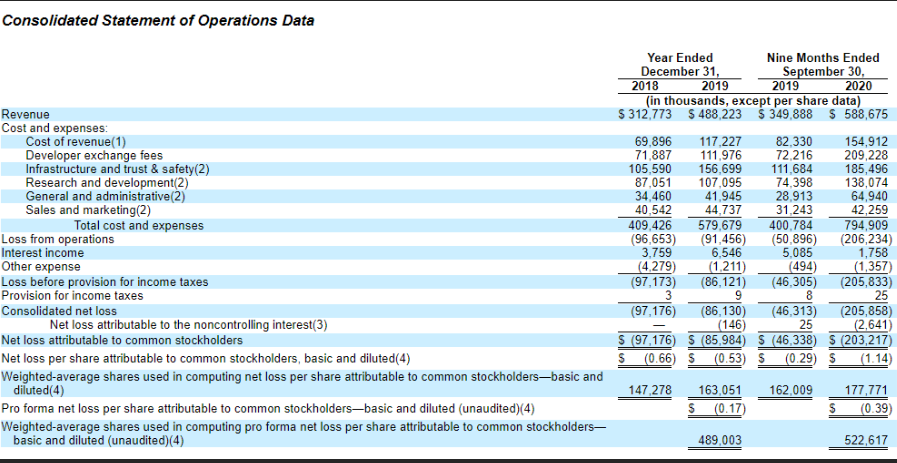

However, almost all the cost line items except for Sales & Marketing grew faster than revenue recently which caused a spike in operating losses to over $200mln in the 9M to Sept 2020. The market will certainly be looking to them to get the cost base under control as revenue scale and prove there is operating leverage in the business.

Concentration

The company doesn't detail what the concentration of play is on their platform. But after doing some digging around Twitter I can see that the developer of Adopt Me!, which is the largest game on Roblox is claiming that 1/3 of the DAUs of Roblux play their game. I haven't seen any more data to back this up but would certainly be an area of questions for the management. Having spent some time on the platform though, I suspect that whilst there will always be a concentration of traffic within some bigger games, as long as new games are being developed and can be intelligently promoted to give them a diverse bench, this shouldn’t be a big problem.

Growth & future considerations

Premium subscriptions - is a promising area to focus on which isn’t significant yet. This revenue stream would certainly command a higher multiple than the one-off purchases being made today. We don't have enough evidence that this is the case yet.

Age expansion - In order to get to the kind of multiple that Unity is trading at (30x sales) we need to see Roblux adding experiences and content for older people. It is clearly much harder to monetise very young children and they are yet to prove they can appeal to an older audience.

Increasing the base - of users that are buying Robux. In their S1 the company says "Only a small portion of our users regularly purchase Robux through subscriptions and pay for experiences and virtual items compared to all users who use our platform in any period". 67% of DAUs are outside the United States and Canada and 68% of purchases of Robux (which, in turn, are bookings) are largely based in the United States and Canada. In other words,** the majority of the bookings (68%) are driven by a minority of the DAUs (33%) and, more importantly, the minority of the DAUs are located in the United States and Canada.

International - They have announced an interested JV in China with Tencent who is awaiting on its publishing license for the platform. But this could be a huge source of growth and a catalyst if it’s approved. If they can focus on the educational element of the game, parents would certainly be much happier allowing kids to play Roblox than League of Legend.

Other types of content monetisation - Following in the footsteps of Fortnite which held a Travis Scott concert in their game. Roblox held a Lil Nas concert in their game as well. Digital merchandise, avatars and other items were available to purchase. The concert was a huge hit and generated 33 million views. Would love to see more of these events and prove out a more diverse revenue base and reason for kids to spend even more time on the game.

Monetisation - Other forms of monetisation such as advertising are still in the early stages and would look for more proof points.

Valuation

Roblox is mooted to IPO for $8bln. This is far too cheap based on comparable multiples. Unity is trading at 30x sales, Roblux should trade at least 15x bookings (discount for all the negatives highlighted above). Assuming we discount for the COVID bump and bookings normalise from ~$2bln to $1.6/1.7bln, the stock could trade up to $24bln.

Note that I haven’t modelled the company which would be a far more robust way to assess valuation.

(Disclosure: I am long Unity)

References

https://www.sec.gov/Archives/edgar/data/1315098/000119312520298230/d87104ds1.htm

https://seekingalpha.com/article/4394513-roblox-and-dispersal-of-creativity

https://seekingalpha.com/article/4391279-roblox-isnt-in-video-games-social-gaming-company