Meta - The Great Metaverse transition

Meta - The Great Metaverse transition

Can Zuck pull it off a third time?

Despite his critics, Mark Zuckerberg has steered the Facebook ship away from two huge rocks that threatened to sink HMS Facebook. The first was in 2012 when they had to shift users from desktop to Mobile. Commentators doubted their ability to move 1bln users from desktop mobile and called for the death of Facebook. The stock dropped around 40% as the shift was also occurring around the time of their controversial IPO. During this move, they bought Instagram, and the rest is history.

The second more subtle shift, which continues today, was in the summer of 2018 when they launched Stories as Snapchat was "snapping" their heels and threatening the dominance of Instagram. The stock fell 40% from July 2018 to Dec 2018 and traded as low as 8x forward EBITDA. Investors once again wrote them off.

I asked my Linkedin followers for their views of Meta and very few companies produce such a visceral (bad) response.

Every stock has its price, and despite the issues and bumpy road ahead, the stock is just too cheap to ignore (Not investment advice)

The problem

Today, Meta is facing a battle, the likes of which they have never faced. They have 3.6bln users, 98% are mobile and there are two direct threats. Firstly is TikTok, and the other is an early and unclear platform shift to Metaverse. All of this whilst the core business’s user growth has ground to a halt.

TikTok has highlighted two critical problems with Facebook. The known issue is that young people don't use or like Facebook. The second issue that is becoming clear is that social media as we knew it before really served two purposes (a) connecting with your friends and family (b) entertainment. TikTok is not a tool for connecting you to your friends and family; it is a tool for showing your creativity and being entertained. Oh boy, is it entertaining! I regard myself as having a lot of self-control, but TikTok is so dangerous that it is the first app that I have ever had to delete off my phone because I was wasting so much time on it. In a rare acknowledgement, Mark has recognised the threat and said that TikTok "continues to grow at quite a faster rate off of a very large base."

So what is the issue? Surely he just copies it and moves on, right? Not so easy. Meta launched Reels, and it has great traction, but it feels like it's too little too late to destroy TikTok; it's more of a defensive move than offensive. The problem is that whilst Tiktok has 1.2bln users, TikTok's monetisation rate is meagre (an estimated $0.06 per hour in the US compared to FB's current average of ~$0.60). Meta needs to be careful. Even if it switches on monetisation, it needs to ensure it doesn't cannibalise its existing ads business.

TikTok competition combined with an already massive user base has resulted in slowing user growth. Daily active users last quarter were flat to down across the world compared to the quarter before.

Is there something more tactical going on?

Quite a lot of commentary has focussed on whether Meta's last quarter results highlighted multiple times that Meta losing users to TikTok would help their antitrust case in terms of how the FTC defined the social media market. It certainly seems that the FTC's arguments have been weakened.

Meta has always had multiple monetisation levers it can pull. This has been the ever dangling carrot for equity investors (fintech, e-commerce, monetisation of Whatsapp etc.). Today, almost all their revenue still comes from advertising, and that business is under threat. Changes in what data Apple users are sharing with apps means that people are opting out of being tracked, and that is impacting how effective Meta's ads are. The singular focus that Mark has had since hiring Cheryl Sandberg on advertising is now being exposed. It is a one-trick pony that needs to find another trick and fast.

The headwinds are real

Apart from slowing user growth from ol’ Blue, the next couple of quarters could be tough as we lap COVID.

One thing that a lot of tech companies have done is pull the pin on Russia and one thing that almost all analysts have done is not change their numbers at all. Given how sensitive Mr Market is to revenue misses and guide downs, we should watch out for Meta’s guidance on Russia as I am sure it’s not immaterial.

Mark has always gone after the user. Monetisation be damned. Quite frankly that has always proven the right strategy. But once again are analysts’ forecasts prepared for a drop in monetisation? Nope. I do wish there was a street-wide recognition of lower monetising Reels being rolled out and cannibalising existing revenue, because then one could at least bet that it won’t cannabalise and this could be incremental revenue. Right now Reels is driving most of Instagram’s growth that is both a good and bad thing.

So what could those new tricks be?

WhatsApp monetisation - We are in the early days of seeing the result of Whatsapp business, but it is clearly a huge area that remains woefully underutilised and monetised. The promise of everything from customer support to restaurant ordering has been there for years but remains elusive. Meta’s focus on making Whatsapp a business CRM is a good first step but still so much more they could do.

Fintech - Google has shown through Google Pay what can be achieved in India with some focus. Google pay is not an app that people have open each day and should not have even had the right to win. Whatsapp is and should have been the payment method of choice, just like WeChat is in China. Instead, Meta made an abortive jump in crypto before even solving the fundamental issue of not being able to pay friends and businesses through any of it's properties.

Reels App - moving Reels into its own app could potentially alleviate some fear of advert cannibalization and could then be an interesting head to head vs Tik Tok.

Advertising - Will we see advertising effectiveness go down due to the rule changes at Apple that have meant users opting out of being targetted? Yes. Will it mean that companies that rely on targeted ads will see customer acquisition costs go up? Yes! Will that mean that people won’t use Facebook anymore to advertise? Nope. It is still one of the best ad companies out there, they may need to hire more AI engineers to infer things vs know things for sure (much like Google) but I am not a believer in a collapse in Meta’s Ads biz.

Metaverse - Meta is spending $25bln+ this year on this next platform to Metaverse. That is more than Apple's entire R&D budget. Now, as you know I am huge believer in this platform shift. The popular belief is that Meta’s version of Metaverse is an Oculus driven, walled garden, VR driven Metaverse. If that was the case (a) you don’t need to spend that much money and (b) it would be money down the drain. Even if we see a cheap Oculus (sub $200), analysts say that will only sell 20mln plus units in 3-5 years. Not enough for developers to make interesting applications en masse. What I hear from my Meta friends is that actually what Mark is working on is more of an open platform, not a closed garden. This would need a huge internal culture shift and questions around whether they can attract people to connect and develop on the platform. A lot of trust would need to be built first.

But….and here is the punchline

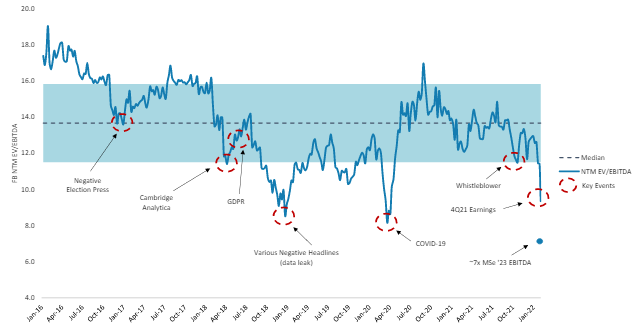

Like quite a few big tech companies it is CHEAP as all hell. It is trading at 13x 2023 PE (yes that is right, close to single-digit earnings) Even if we see some cannibalization in ads it’s cheap. Also, it is on under 6x EBITDA which is growing at 21%. The stock has literally never been cheaper.

We may be in for a bumpy year with the company at this price not a lot of things need to go right for you to make money. Nonetheless, here is a checklist of things to watch out for

Can Meta…

(a) attract top-rated talent despite the noise around the company

(b) Navigate this next platform shift without losing focus on the core business / destroying tonnes of value

(c) monetise the unmonetised properties

(d) defend itself from TikTok through whatever means necessary (go after the users)

Facebook valuation